Is Credit Card Installment Or Revolving

Is Credit Card Installment Or Revolving - Unlike an installment loan account, revolving credit accounts generally finance smaller, ongoing individual purchases. Credit cards, department store cards, gas cards, other retail cards, and home equity lines of credit. A revolving account gives you access to an always available credit line, which determines how much you can charge to that account at any given time. Revolving credit allows you to borrow money up to a set credit limit, repay it and borrow again as needed. Revolving credit allows borrowers to spend the borrowed money up to a predetermined credit limit, repay it, and spend it again. A consumer who opens a credit card agreement or another revolving credit account is not automatically assuming a debt.

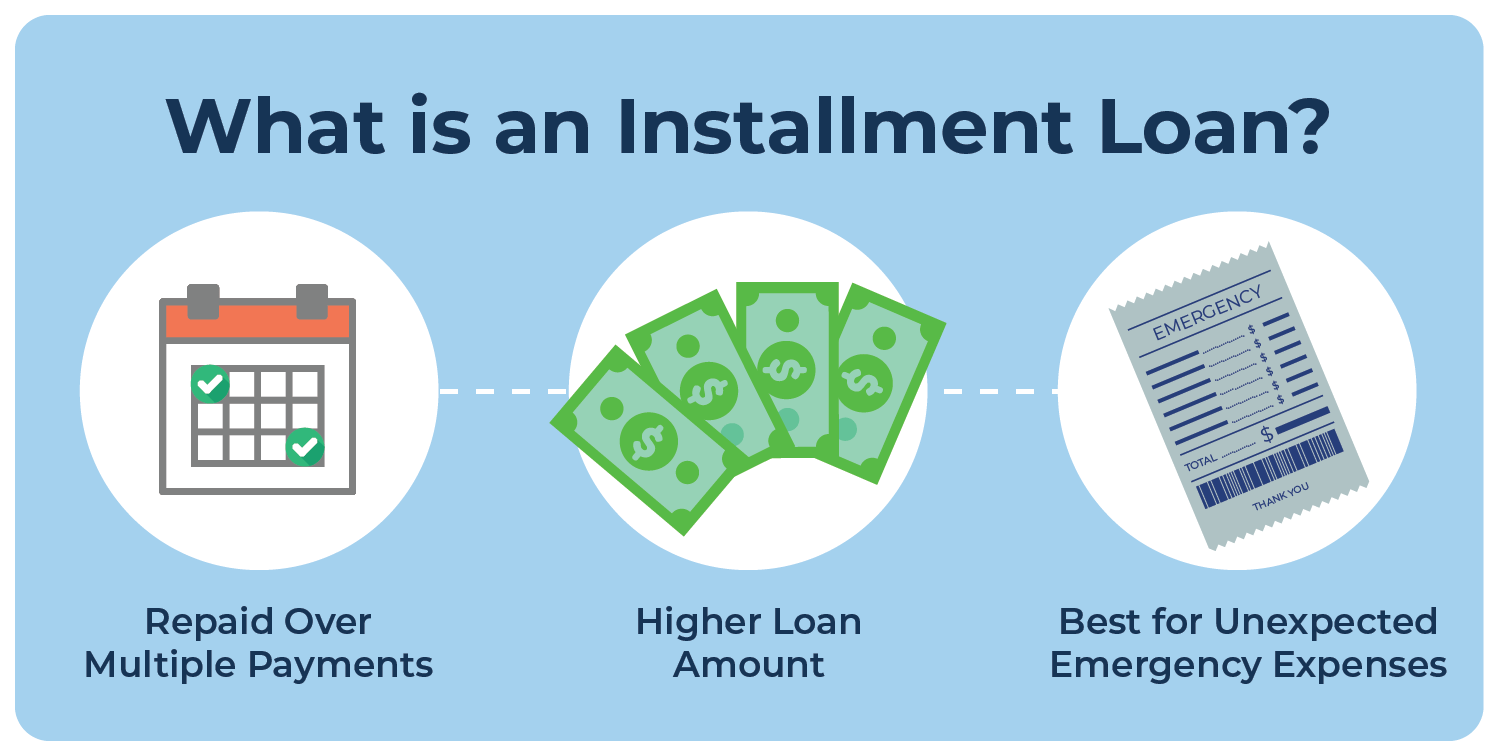

With installment credit, the borrower receives a lump sum of. By contrast, installment credit lets you borrow one lump sum, which you pay back in scheduled payments until the loan is paid in full. A consumer who opens a credit card agreement or another revolving credit account is not automatically assuming a debt. Credit cards are a common and widely used form of revolving credit. Depending on how responsibly they’re used, credit card payments can positively or negatively affect credit ratings.

Understanding Installment vs Revolving Credit for Canadians BHM Financial

Credit cards, department store cards, gas cards, other retail cards, and home equity lines of credit. To make the most of both, you’ll need to. Banks, lenders, and retailers may provide lines of. A consumer who opens a credit card agreement or another revolving credit account is not automatically assuming a debt. Revolving credit also includes the following:

Revolving Credit Installment Credit What's The Difference?, 58 OFF

Depending on how responsibly they’re used, credit card payments can positively or negatively affect credit ratings. Credit cards, department store cards, gas cards, other retail cards, and home equity lines of credit. The two most common types of credit accounts are installment credit and revolving credit, and credit cards are considered revolving credit. Banks, lenders, and retailers may provide lines.

Installment Loans vs. Revolving Credit Lexington Law

The two most common types of credit accounts are installment credit and revolving credit, and credit cards are considered revolving credit. Installment loans (student loans, mortgages and car loans) show that you can pay back borrowed money consistently over time. With installment credit, the borrower receives a lump sum of. Revolving credit allows borrowers to spend the borrowed money up.

How does a private credit fund work? Leia aqui Are private credit

By contrast, installment credit lets you borrow one lump sum, which you pay back in scheduled payments until the loan is paid in full. Here, an agreement is made between a bank and a customer, and a maximum credit limit is set with specific minimum repayment conditions. Unlike an installment loan account, revolving credit accounts generally finance smaller, ongoing individual.

Why does my credit card say I have an installment loan? Leia aqui Why

Revolving credit also includes the following: Banks, lenders, and retailers may provide lines of. Credit cards are a common and widely used form of revolving credit. Depending on how responsibly they’re used, credit card payments can positively or negatively affect credit ratings. Revolving credit allows you to borrow money up to a set credit limit, repay it and borrow again.

Is Credit Card Installment Or Revolving - With installment credit, the borrower receives a lump sum of. Unlike an installment loan account, revolving credit accounts generally finance smaller, ongoing individual purchases. Here, an agreement is made between a bank and a customer, and a maximum credit limit is set with specific minimum repayment conditions. Credit cards are a common and widely used form of revolving credit. Meanwhile, credit cards (revolving debt) show that you can take out. Revolving credit also includes the following:

Credit cards are a common and widely used form of revolving credit. Revolving credit also includes the following: A revolving account gives you access to an always available credit line, which determines how much you can charge to that account at any given time. A consumer who opens a credit card agreement or another revolving credit account is not automatically assuming a debt. With installment credit, the borrower receives a lump sum of.

Banks, Lenders, And Retailers May Provide Lines Of.

The two most common types of credit accounts are installment credit and revolving credit, and credit cards are considered revolving credit. Revolving credit allows you to borrow money up to a set credit limit, repay it and borrow again as needed. Credit cards, department store cards, gas cards, other retail cards, and home equity lines of credit. To make the most of both, you’ll need to.

With Installment Credit, The Borrower Receives A Lump Sum Of.

A consumer who opens a credit card agreement or another revolving credit account is not automatically assuming a debt. A revolving account like a credit card or home equity line of credit (heloc) differs from an installment loan. Mortgages, auto loans, student loans, personal loans, and home equity loans. Revolving credit can be used continually while installment credit is finite in its terms.

Revolving Credit Allows Borrowers To Spend The Borrowed Money Up To A Predetermined Credit Limit, Repay It, And Spend It Again.

A revolving account gives you access to an always available credit line, which determines how much you can charge to that account at any given time. Revolving credit also includes the following: Depending on how responsibly they’re used, credit card payments can positively or negatively affect credit ratings. Unlike an installment loan account, revolving credit accounts generally finance smaller, ongoing individual purchases.

Credit Cards Are A Common And Widely Used Form Of Revolving Credit.

Meanwhile, credit cards (revolving debt) show that you can take out. Installment loans (student loans, mortgages and car loans) show that you can pay back borrowed money consistently over time. By contrast, installment credit lets you borrow one lump sum, which you pay back in scheduled payments until the loan is paid in full. Here, an agreement is made between a bank and a customer, and a maximum credit limit is set with specific minimum repayment conditions.